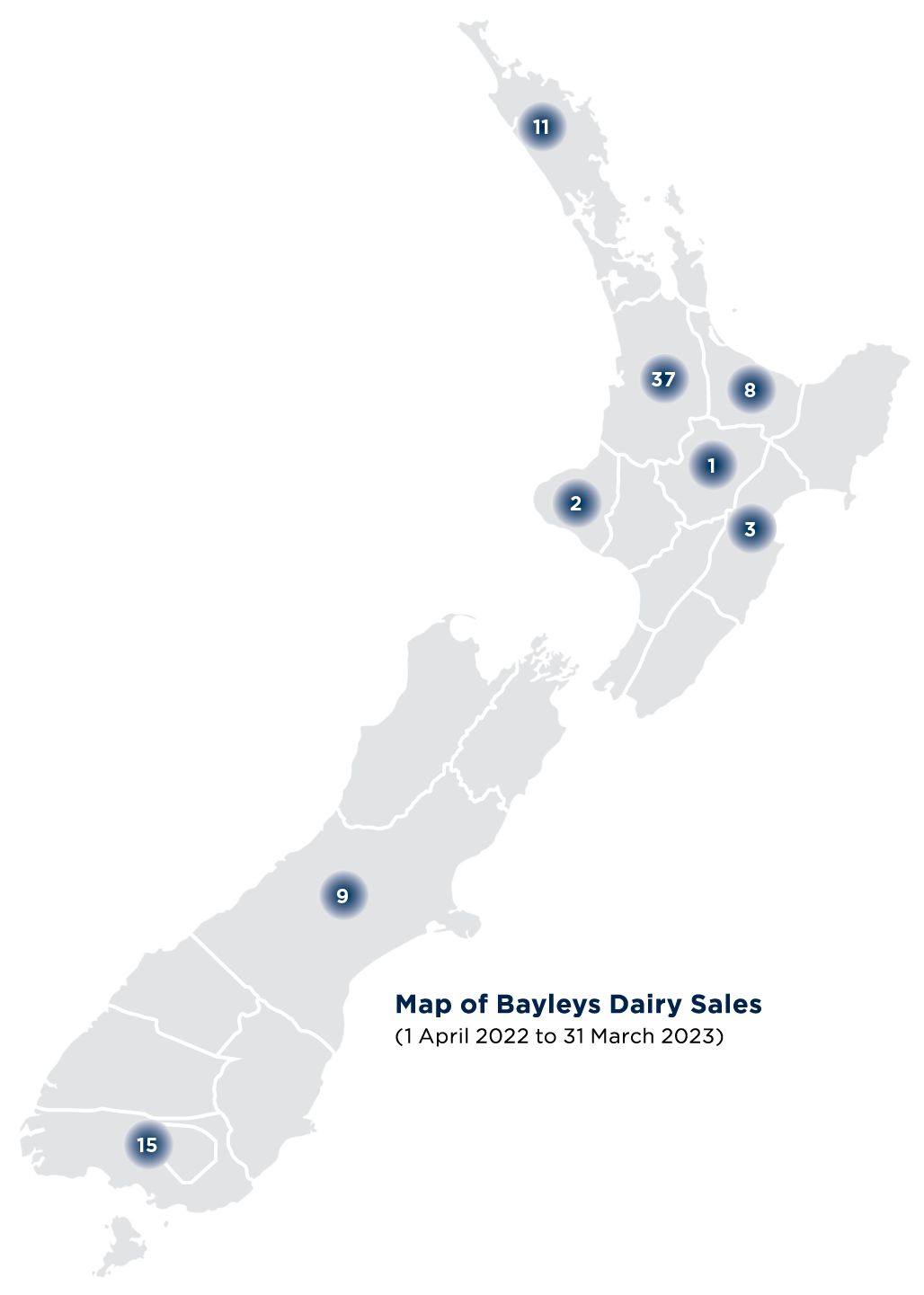

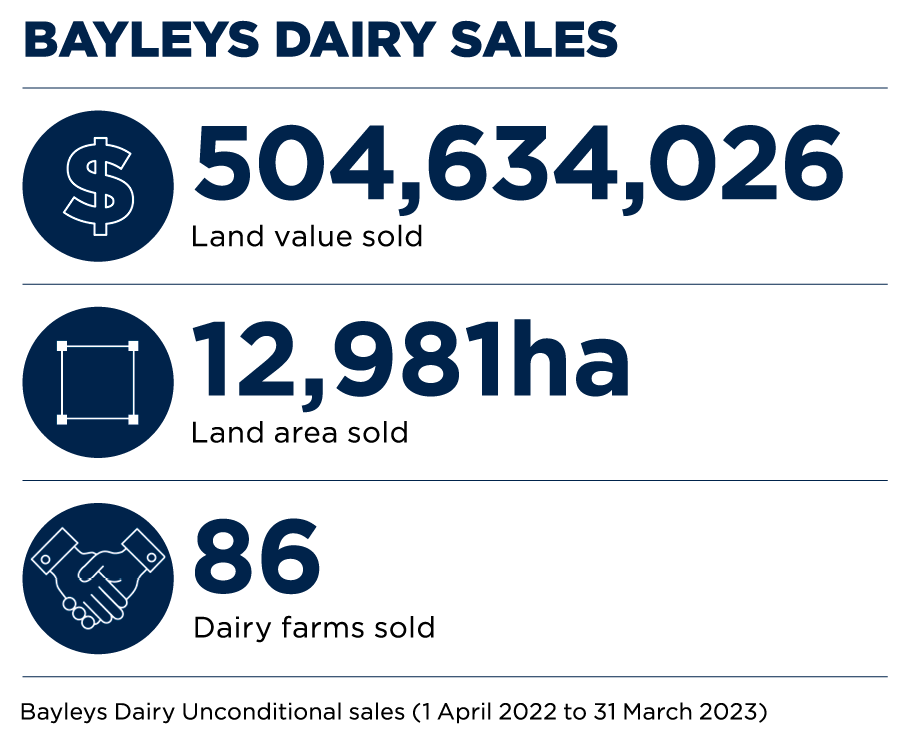

Rural Insight -

Dairy market update – June 2023

Biggest trends

Margins being squeezed

The softening farmgate milk price forecast together with operating cost inflation is squeezing margin and has slowed the rate of activity in the market.

Environmental due diligence the new normal

Buyers and lenders continue to place high reliance on environmental information to assess the potential impact on future production and/or CapEx required to meet environmental standards.

Flight to quality

With a greater selection of properties available providing more options for buyers, naturally they are becoming more selective. Quality and location of the property remain primary drivers of value.

Outlook for the next 12 months

Restricted land use drives scarcity

In the absence of strong motivating factors (such as age, energy, debt, up/downsize), vendors are likely to remain resilient to any price gap. Restrictions on land use will ultimately drive scarcity of the national total productive platform in the longer term.

Declining sales activity expected to continue

Although confidence in the sector has improved in recent years, investment returns in the immediate term are expected to limit the level of buyer activity. Longer term investment strategies are likely to drive activity along, including decommissioning of smaller dairy farms, given continued demand expected for support land.

Cost of debt will influence market liquidity

While well capitalised operators are expected to be able to continue to access debt, the rate of increase in the cost of debt is expected to reduce the level of overall liquidity circulating in the market.