Rural Insight -

Rural Insight viticulture market sector report H1 2023

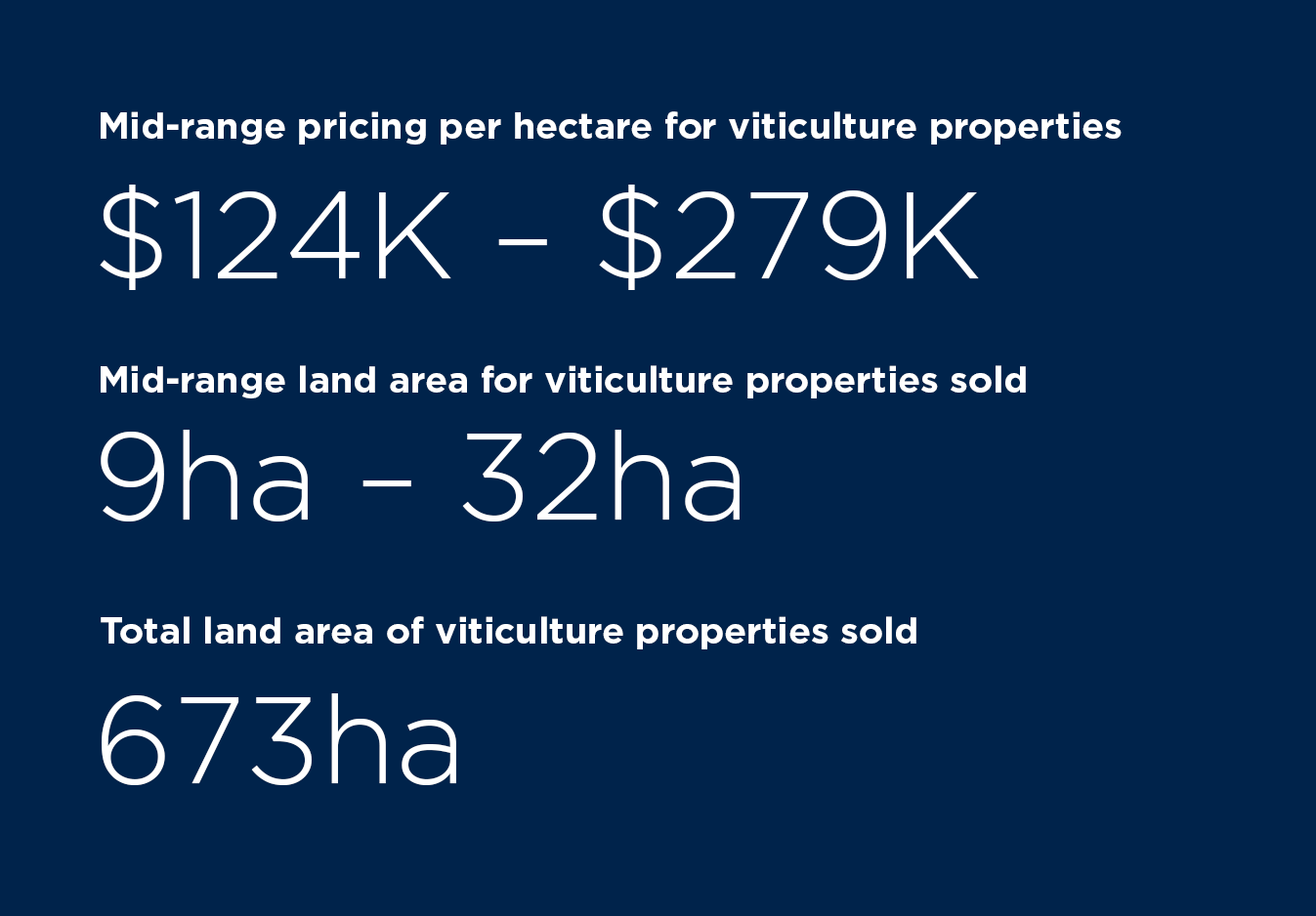

See below for a summary of the biggest trends in the viticulture market, plus an outlook on the next 12 months.

Biggest trends

Sauvignon Blanc is the main cash cow

Market remains primarily focused on securing supply of Sauvignon Blanc grapes. Given global consumer demand has continued to outstrip supply, with this year’s yield volume said to be “about average”, quality is expected to provide for one of the best vintages in recent years. Production capacity remains a key driver of value.

Spread of offering remains attractive

Vineyards producing a range of quality varietals remain attractive. Being typically smaller, production is focused on quality. Specialist organic production or leveraging the established sustainability practices by the wine industry provide opportunity, particularly for high-end brands wanting to achieve a premium and/or differentiated product offering.

Vine replacement a focus

Many vineyards are now approaching 30 years. Where production is reducing or becoming uneconomic, redevelopment or ‘refreshing the asset’ with new plantings is occurring. CapEx and/or operational advantages are key considerations, particularly where vines have tighter spacing and able to drive productivity gains.

Outlook for the next 12 months

Focus on securing supply for growth export markets

Strong demand forecast in the US market in the medium term remains, and alongside constrained supply of land available in Marlborough, vineyard buyers will continue to focus on securing supply of Sauvignon Blanc. Expansion is expected into regions where scaled development opportunity exists for Sauvignon Blanc, Pinot Gris and Pinot Noir.

Hands off investment will remain attractive

Given the relatively scalable and systemised nature of vineyards, it provides opportunity for a wider investor pool. Contract management remains competitive and provides opportunity for smaller through to corporate buyers, as they adjust to a higher cost of debt environment.

Lifestyle purchasers will remain persistent

Activity from lifestyle purchasers is expected to remain, particularly in the $2.5M to $5.0M price range. The opportunity to generate passive income alongside the lifestyle amongst the vines will continue to appeal to those searching for a home and supplementary income.