Rural Insight -

Rural Insight pastoral market sector report H1 2023

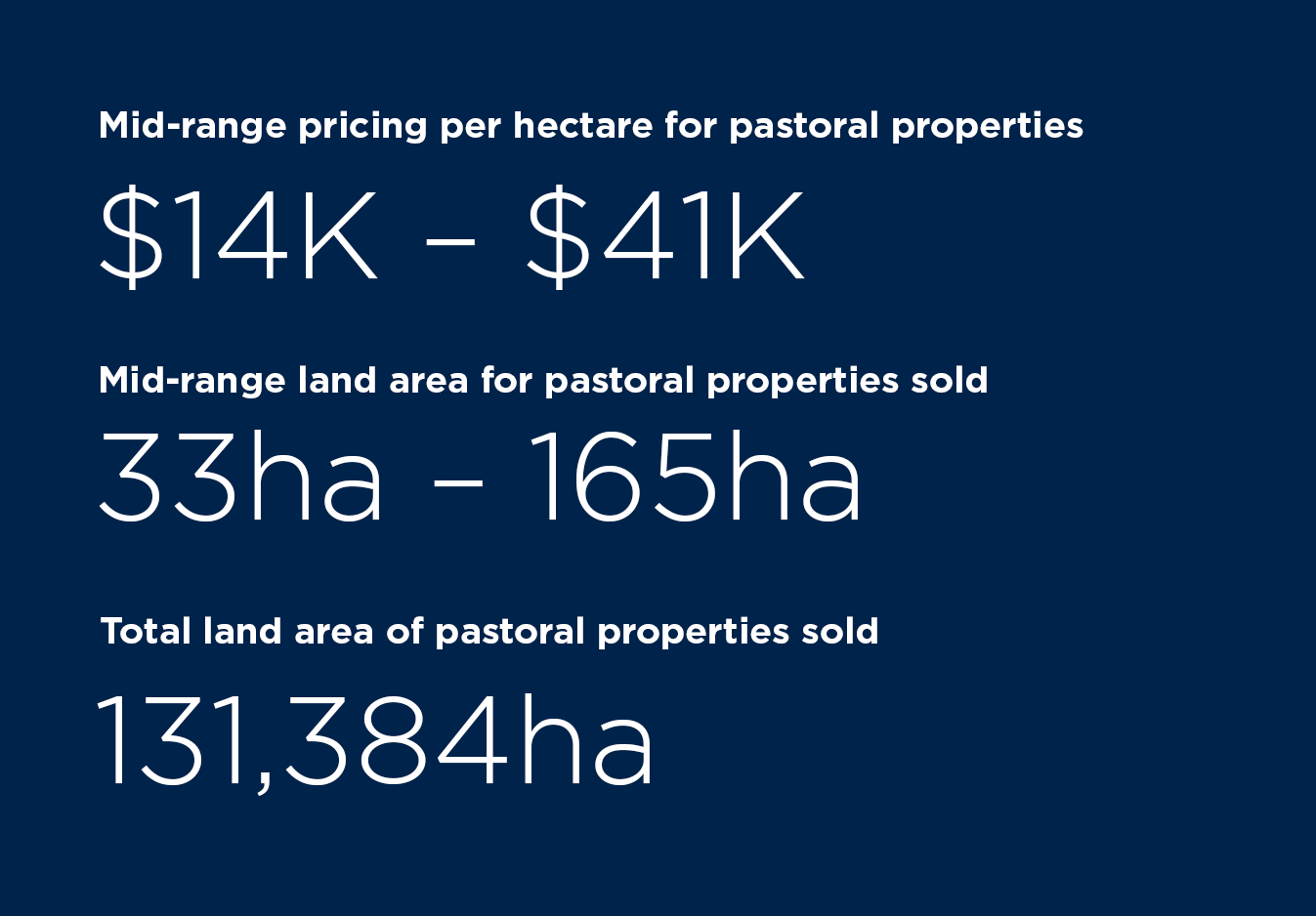

See below for a summary of the biggest trends in the pastoral market, plus an outlook on the next 12 months.

Biggest trends

Margin compression slows activity

With red meat commodity prices coming off their peak, together with accretive costs incurred on farm, margins are being compressed. Affordability is now heavily influenced by the accelerated increase in the cost of debt seen in the past 12 months.

Environmental standards add due diligence

While more acute in the dairy sector, pastoral buyers remain alert to compliance with environmental standards, despite recent regulatory indecision. Vendors should have quality documentation available to assist saleability, particularly for the higher value properties that may attract more scrutiny.

Less competing land use pressure

Competing land use amongst the sub-sectors remains, but at a lesser amount of intensity than in recent periods. Dairy farmers seeking additional support land as part of their strategy to meet environmental standards remain active, with competition from fattening operators reducing. Conversion of hill country to forestry has been dampened due to regulation and volatility in the NZU carbon price.

Outlook for the next 12 months

Pressure on forestry conversion

Buyer activity for hill country conversion to forestry started to slow spring 2022, initially influenced by conversion restrictions on offshore buyers. Forestry conversion activity is expected to continue, but less aggressively given the recent forestry slash review (albeit focused primarily on the North Island East Coast). The recommendations are expected to have a more controlling influence on land use.

Motivation to transact will be tested

Vendors who do not have motivating factors to transact are expected to remain resilient to price adjustment pressure. The anticipated reduction in competing land use from forestry would provide opportunity for buyers of hill country for breeding operations after having been arguably priced out of this market in more recent times.

Thinner buyer pool with increased options

Buyer willingness will continue to be heavily influenced by their capacity and affordability assessment. Market activity is therefore expected to continue to soften with activity likely to be associated with better quality properties, strategic acquisitions or where there is a perceived value gain as a result of more immediate motivating factors of vendors (such as age, energy, debt or up/downsize plans).